POSTED

October 31, 2025

What Is the Difference Between ESG Investing and Socially Responsible Investing?

What is ESG and SRI? While both refer to a more sustainable approach to investing, there are key differences between the two. This article dives into the differences and outlines how each can be used to fully align your investment portfolio with your vision.

The terms “ESG investing” and “Socially Responsible Investing” (SRI) often appear interchangeably in financial media, investment marketing materials, and casual conversation about sustainable finance. This conflation creates confusion for investors trying to align their portfolios with their values or sustainability goals. While both approaches consider factors beyond pure financial returns, they represent fundamentally different philosophies, methodologies, and implementation strategies.

Understanding these distinctions matters practically for investors. ESG and SRI lead to different portfolio compositions, risk-return profiles, and alignment with personal or institutional objectives. An investor seeking to avoid companies that conflict with their moral values needs a different approach than one looking to identify companies best managing sustainability-related risks. As sustainable investing assets reach unprecedented scales, clarity about these approaches becomes essential for making informed investment decisions.

What Is ESG Investing?

ESG investing integrates environmental, social, and governance factors into traditional investment analysis to better assess risks and opportunities. Rather than replacing financial analysis, ESG investing enhances it by incorporating material sustainability factors that affect long-term performance. The approach recognizes that companies managing ESG factors well often demonstrate superior risk management, operational efficiency, and strategic positioning.

The key distinction of ESG investing lies in its framework and methodology. ESG operates as an inclusion-based approach, evaluating all companies within a sector on how well they manage relevant sustainability factors. A fossil fuel company with strong safety records, robust governance, and improving emissions intensity might score well on ESG metrics relative to peers, even though its core business involves carbon-intensive activities. This relative assessment allows investors to maintain broad market exposure while tilting toward better-managed companies within each sector.

The act of standardization defines ESG investing’s analytical approach. Frameworks from organizations like the Sustainability Accounting Standards Board (SASB) identify financially material ESG factors by industry. Rating agencies like MSCI and Sustainalytics score companies using consistent methodologies, enabling comparison across thousands of securities. This standardization allows ESG integration into quantitative models, index construction, and systematic portfolio management.

The regulatory environment increasingly supports ESG investing through disclosure requirements and reporting standards. The Task Force on Climate-related Financial Disclosures (TCFD) provides frameworks for climate risk reporting, while jurisdictions worldwide implement mandatory ESG disclosure rules. This regulatory backing creates the data infrastructure that enables systematic ESG analysis across entire markets.

For a more detailed look on ESG Investing and the standardization metrics, check out our article “What Are ESG Metrics and Why Do They Matter?”

What Is Socially Responsible Investing?

Socially Responsible Investing (SRI) predates ESG by decades, emerging from faith-based investing traditions that avoided “sin stocks” like tobacco, and alcohol. Modern SRI has evolved beyond simple exclusion but retains its foundation in moral and ethical considerations rather than purely financial analysis.

Socially Responsible Investing fundamentally operates as a values-based framework where investors actively choose investments that align with their principles. This approach typically involves negative screening—excluding companies or sectors that conflict with specific ethical criteria. An SRI investor might exclude all fossil fuel companies regardless of their relative ESG performance, or avoid pharmaceutical companies that conduct animal testing irrespective of their governance quality or social impact in other areas.

The evaluation process in SRI relies on principles rather than standardized metrics. While an ESG approach might score a tobacco company on employee safety and supply chain management, an SRI approach might exclude it entirely based on the principle that tobacco products harm public health. This principles-first methodology means SRI portfolios often look substantially different from broad market indices, accepting tracking error in exchange for values alignment.

Positive screening in SRI actively seeks companies making beneficial social or environmental impact. Unlike ESG’s relative scoring within sectors, SRI’s positive screening might concentrate investments in renewable energy, affordable housing, or community development financial institutions. This intentional concentration on “good” companies or sectors distinguishes SRI from ESG’s sector-neutral approach.

What are the Key Differences and Why Do They Matter?

These differences translate into tangible portfolio implications that investors must understand. An ESG approach typically results in portfolios that maintain similar sector weightings to broad market indices, potentially reducing tracking error and maintaining diversification benefits. This means an ESG investor might still hold energy sector exposure through companies with strong environmental management systems, even if those companies extract fossil fuels. The performance correlation with traditional benchmarks remains high, making ESG integration easier for institutional investors with specific benchmark-relative return targets.

SRI portfolios, by contrast, can look dramatically different from market indices. Excluding entire sectors like fossil fuels, or tobacco can lead to significant sector concentration. This concentration can amplify both risks and returns. During periods when excluded sectors underperform, SRI portfolios might outpace benchmarks. However, when excluded sectors rally, SRI investors may experience substantial underperformance relative to traditional indices.

Methodologically, ESG relies on standardized metrics and quantitative scoring systems that enable systematic comparison across investments. Companies receive ESG scores based on disclosure quality, performance metrics, and management practices. This standardization allows for integration into passive strategies, smart-beta products, and quantitative models—expanding access and reducing costs. SRI employs qualitative assessments based on ethical frameworks, often making binary include/exclude decisions rather than scoring companies on a spectrum. This approach typically requires active management, potentially affecting fees and tax efficiency.

The liquidity implications differ as well. ESG strategies that maintain broad market exposure typically preserve liquidity characteristics similar to traditional portfolios. SRI strategies that concentrate in specific themes or exclude major market segments could face potential liquidity constraints, particularly during market stress when correlations increase and diversification benefits matter most. For large institutional investors, the inability to invest in certain sectors due to SRI constraints can create significant implementation challenges when deploying capital at scale.

Understanding these differences helps investors to set realistic expectations and choose appropriate strategies. Those prioritizing market-rate returns with enhanced risk management might prefer ESG integration. Investors willing to accept tracking error and potential return variation to align investments with their principles might choose SRI. A lot of investors opt to combine both approaches—using ESG integration as a baseline while applying selective SRI screens for the most objectionable industries.

Both approaches serve important roles in sustainable investing. ESG provides a framework for mainstream integration of sustainability factors, enabling large institutions to incorporate these considerations without dramatic portfolio restructuring. SRI offers a mechanism for investors with strong ethical convictions to ensure their capital doesn’t support activities they oppose, even if this means accepting different risk-return profiles.

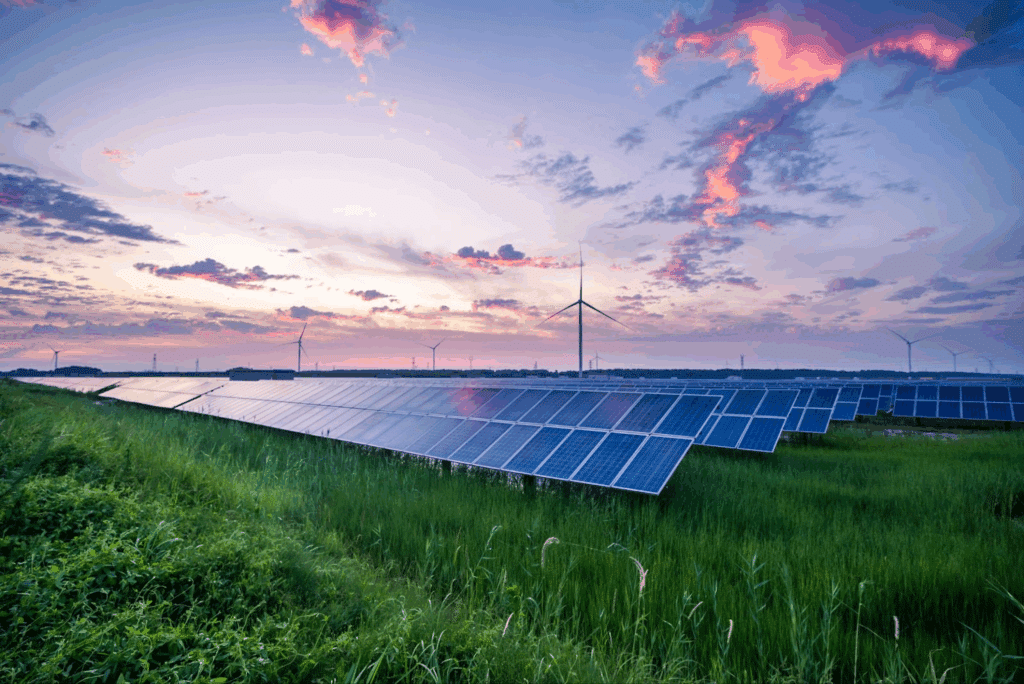

How They Relate to Utility-Scale Solar Investments

Utility-scale solar investments demonstrate how ESG and SRI perspectives can converge on the same opportunity for different reasons. From an ESG perspective, solar projects score well across all three pillars. Environmentally, they generate clean electricity with minimal lifecycle emissions—NREL research indicates solar PV achieves approximately 40-50 grams of CO2 equivalent per kilowatt-hour over its lifetime, compared to 820 grams for coal and 490 grams for natural gas. Socially, these projects create local jobs and tax revenue for their local communities and governance-wise, the sector features transparent project development, rigorous third-party engineering reviews, and clear regulatory frameworks.

ESG analysis of solar investments focuses on quantifiable metrics that correlate with financial performance. Land use efficiency (acres per megawatt) affects project costs and permitting complexity. Community engagement quality influences development timelines and operational stability. Water usage metrics matter in drought-prone regions. These ESG factors directly impact project returns, making them material to investment decisions regardless of environmental ideology.

From an SRI perspective, utility-scale solar represents a positive screening opportunity—actively directing capital toward climate solutions. SRI investors might choose solar not just because projects score well on ESG metrics, but because they tend to align with principles of environmental stewardship and intergenerational equity. The sector offers a way to exclude fossil fuels while investing in their replacement, satisfying both negative and positive screening criteria.

The convergence of ESG and SRI perspectives on solar highlights an important point: the best sustainable investments often excel from multiple viewpoints. Utility-scale solar projects don’t require investors to choose between values and value. They can offer strong risk-adjusted returns that satisfy ESG criteria while providing the explicit positive impact that SRI investors seek.

Conclusion

ESG investing and socially responsible investing represent distinct approaches to incorporating sustainability into investment decisions. ESG enhances traditional analysis with material sustainability factors, maintaining broad market exposure while identifying better-managed companies. SRI prioritizes ethical alignment, accepting portfolio concentration or exclusion to match investments with values. Understanding these differences enables investors to choose approaches aligned with their objectives—or combine both strategies for comprehensive sustainable investing.

Utility-scale solar exemplifies how certain investments can satisfy both frameworks simultaneously. These projects can deliver the quantifiable ESG performance that enhances risk-adjusted returns while providing the explicit positive impact that values-driven investors seek. As the sustainable investing landscape continues evolving, clarity about different approaches empowers investors to build portfolios that achieve both financial and non-financial objectives.

For investors interested in opportunities that excel under both ESG and SRI criteria, Shasta Power specializes in developing utility-scale solar projects that aim to deliver strong financial returns alongside measurable environmental and social benefits. Connect with Shasta Power to explore how solar investments can align with your investment strategy, whether driven by ESG analysis, socially responsible principles, or both.